My PRS Holdings

Update: There is currently a campaign on Fundsupermart giving RM40 in credits when you invest RM3,000 in a single transaction: Link hERE.

Referral link: hERE (discount on fees)

I use Fundsupermart as it is easy and I can do everything online. Rates are good as well. However, I do not recommend going over RM3,000 a year as that is the maximum tax relief. You’re still paying fees every year and you know how I feel about them fees.

Below is my updated PRS holding for 2023.

I’ve invested for a few years now.. so the 24% returns are really nothing to shout about. I do RM3,000 every year for the tax relief that’s all.

What is a Private Retirement Scheme (PRS)?

The Private Retirement Scheme in Malaysia was launched approximately 4 years ago back in mid-2012 as a supplement to the Employee’s Provident Fund (EPF) because it was found that most Malaysians relied solely on their EPF for retirement which was severely insufficient. The PRS is a defined contribution scheme which in simple terms – you decide how much you contribute and is regulated by the Securities Commission of Malaysia. The entity that administrates and handles PRS is the Private Pension Administrator (PPA), every Malaysian interested in contributing to PRS is required to create an account with them (more on this later).

Photo source: PPA

Benefits of PRS

So, why contribute to PRS?

PRS Tax Relief

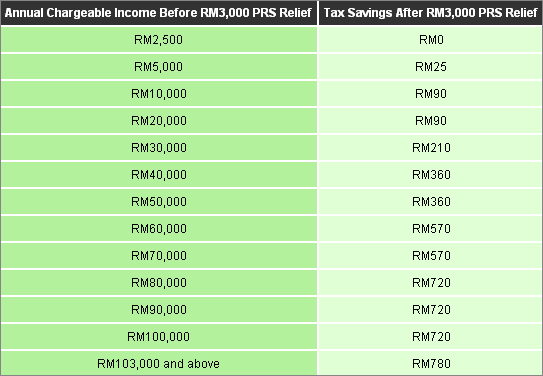

The Malaysian government, in a bid to encourage everyone to fund their retirement provided a few benefits in the form of tax reliefs and a PRS youth incentive. Individuals who contribute to a PRS can enjoy up to RM3,000 tax relief per year of assessment. Many confuse this as RM3,000 saved every year when you contribute.

This is not the case, instead, think of the RM3,000 as the cap, if you invest RM3,001 in a PRS, you only get the relief of up to RM3,000. So, potentially an individual taxed at the highest rate can save up to RM780 per year in taxes if he/she contributed to a PRS. This however makes contributing more than RM3,000 a year unnecessary.

As per the table below, you will notice that the maximum savings an individual can get is RM780, if he is in the highest taxable bracket and is taxed at 26%.

PRS Youth Incentive

The PRS Youth Incentive is an initiative by the Malaysian government to encourage young Malaysians to start saving and investing for retirement. A one-off incentive of RM500 will be contributed by the Government to Malaysian individuals who qualify for the incentive.

Who is eligible?

- Malaysian citizens only;

- Aged between 20-30 years;

- A minimum gross investment amount of RM1,000 must be accumulated in a single PRS fund of a single PRS provider within a calendar year, between 2014 till 2018

With the above-mentioned incentives, I myself have contributed RM3,000 every year to a Private Retirement Scheme through Fundsupermart. I chose them because prior to PRS, I’ve been investing in Unit Trusts and Mutual Funds through them. Everything is done online and is simple to follow. Some of the forms will require your signature and thus will be mailed/couriered to you. You may sign up for an account here and follow their instructions.

I chose to contribute to the PRS funds as seen below:

There are a total of 8 PRS Providers:

- Affin Hwang Asset Management Berhad

- AIA Pension and Asset Management Sdn. Bhd.

- AmInvestment Services Berhad

- CIMB-Principal Asset Management Berhad

- Kenanga Investors Berhad

- Manulife Asset Management Services Berhad

- Public Mutual Berhad

- RHB Asset Management Sdn. Bhd.

The Disadvantages of a PRS

Yes, I invested in a PRS and the tax relief as well as the RM500 youth incentive wasn’t too bad. However, a Private Retirement Scheme is in essence a Unit Trust / Mutual Fund, and you know how much I hate them here in Malaysia as I’ve mentioned in my previous post Fundsupermart and Unit Trusts in Malaysia. The same ridiculous fees are charged by the providers regardless if you make a profit or a loss. Notice that my total profit averages to a measly 3.15% after 2 whole years, of course this is not including the tax relief afforded by the government.

Furthermore, your money is locked in until you reach the age of 55. Early withdrawal (with tax penalties) is allowed under some circumstances which are all specified at the PPA’s website.

Conclusion

All that being said, I will still continue to contribute RM3,000 each year solely because of the tax relief which I view as a guaranteed return provided by Putrajaya. I am in no way put off by the long wait till I’m 55 because I have surplus savings. However, the same cannot be said for my fellow Malaysians out there who are struggling to make ends meet.

Will you continue to contributed to a PRS this year? Have you taken advantage of the tax incentives provided by our Government?

Thank you for reading.